Aggregated Expectile Regression by Exponential Weighting

An adaptive model combination approach to nonparametric expectile regression

By Yuwen Gu and Hui Zou in Research

September 5, 2019

Gu, Y., & Zou, H. (2019). Aggregated expectile regression by exponential weighting. Statistica Sinica, 29(2), 671–692.

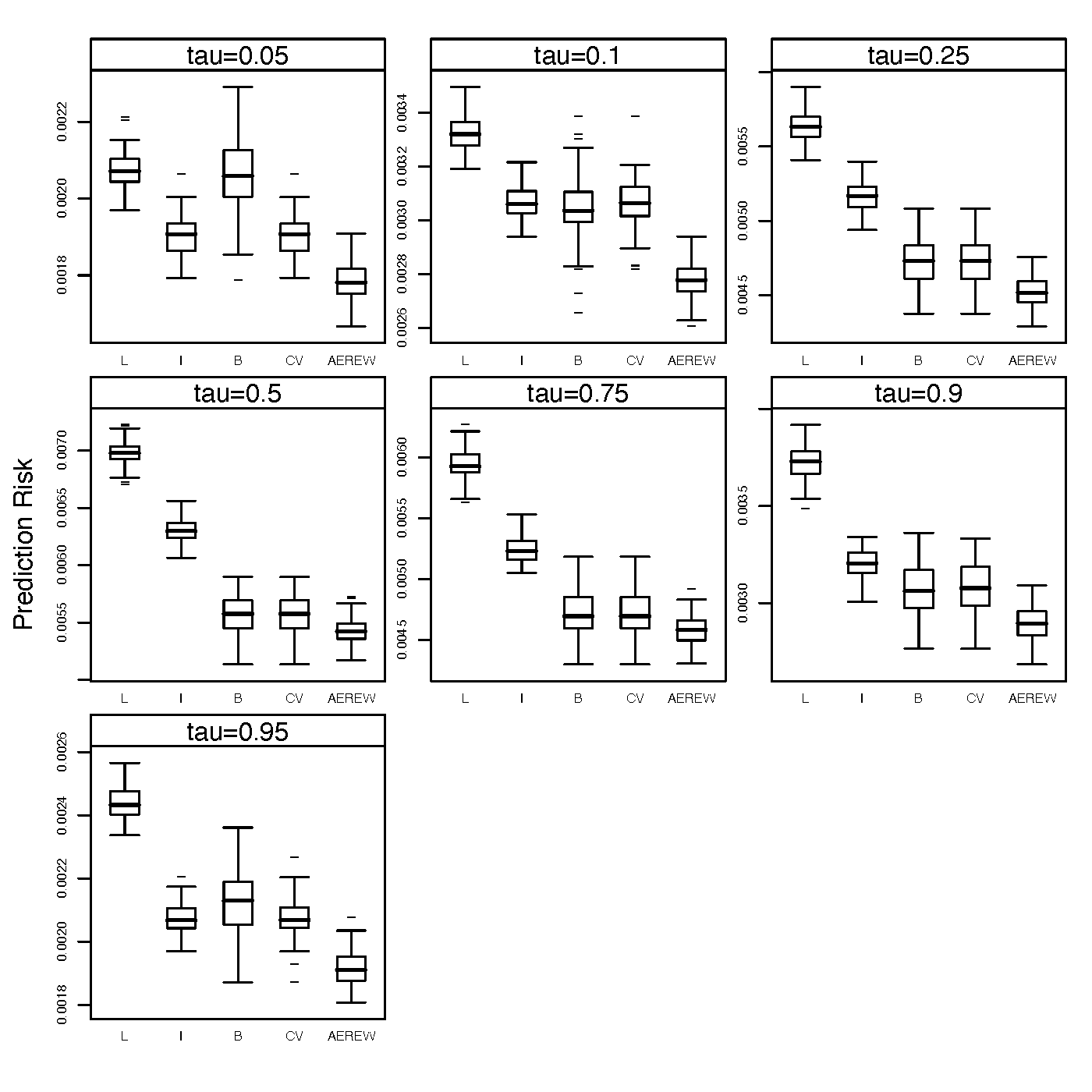

Abstract

Various estimators have been proposed to estimate conditional expectiles, including those from multiple linear expectile regression, local polynomial expectile regression, boosted expectile regression, and so on. It is a common practice that several plausible candidate estimators are fitted and a final estimator is selected from the candidate list. In this article, we advocate the use of an exponential weighting scheme to adaptively aggregate the candidate estimators into a final estimator. We show oracle inequalities for the aggregated estimator. Simulations and data examples demonstrate that the aggregated estimator could have substantial gain in accuracy under both squared and asymmetric squared errors.