Demystifying a class of multiply robust estimators

Multiply robust estimators are doubly robust estimators in essence

By Wei Li, Yuwen Gu, and Lan Liu in Research

December 1, 2020

Li, W., Gu, Y., & Liu, L. (2020). Demystifying a class of multiply robust estimators. Biometrika, 107(4), 919–933.

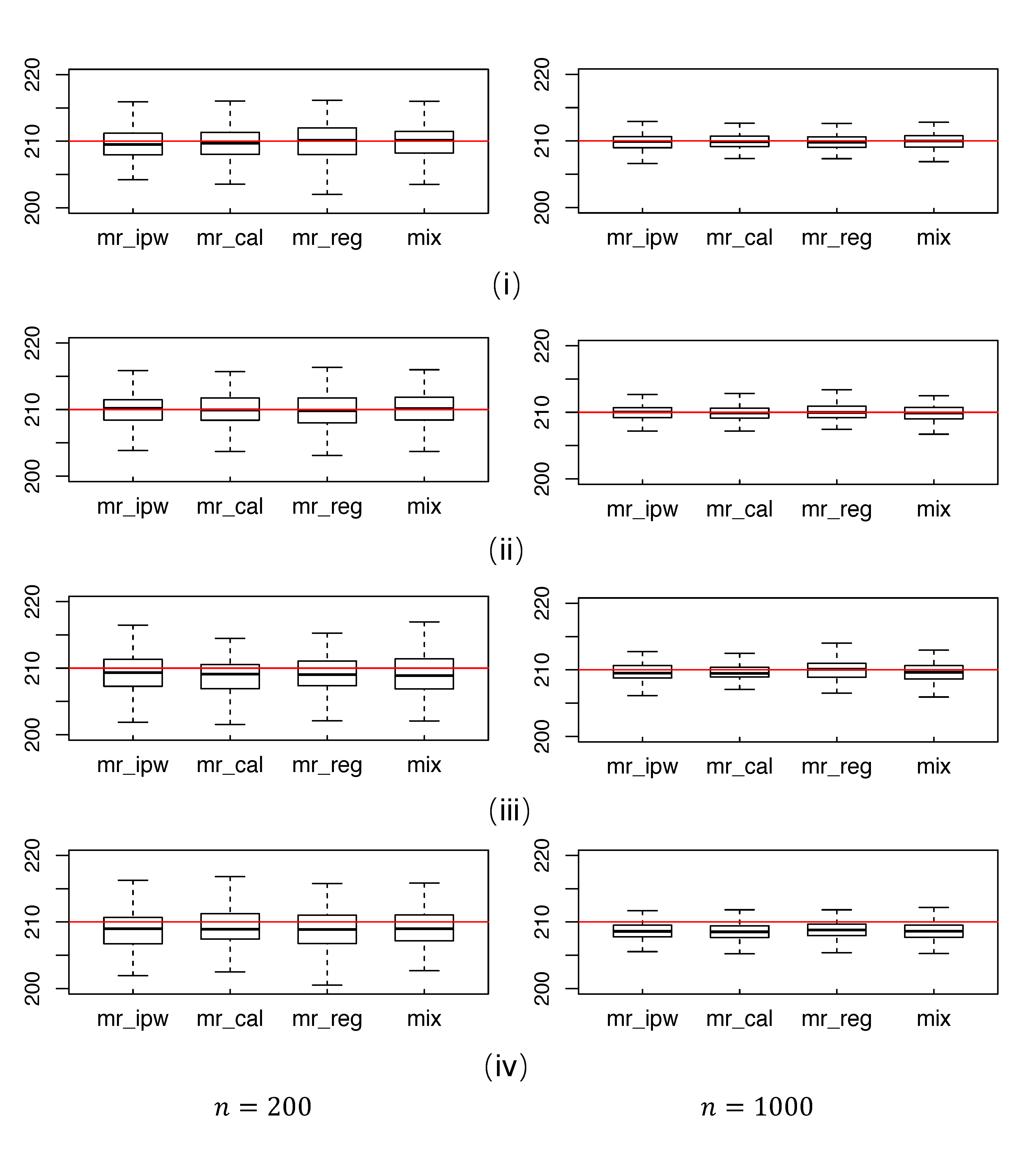

Abstract

For estimating the population mean of a response variable subject to ignorable missingness, a new class of methods, called multiply robust procedures, has been proposed. The advantage of multiply robust procedures over the traditional doubly robust methods is that they permit the use of multiple candidate models for both the propensity score and the outcome regression, and they are consistent if any one of the multiple models is correctly specified, a property termed multiple robustness. This paper shows that, somewhat surprisingly, multiply robust estimators are special cases of doubly robust estimators, where the final propensity score and outcome regression models are certain combinations of the candidate models.To further improve model specifications in the doubly robust estimators, we adapt a model mixing procedure as an alternative method for combining multiple candidate models. We show that multiple robustness and asymptotic normality can also be achieved by our mixing-based doubly robust estimator. Moreover, our estimator and its theoretical properties are not confined to parametric models. Numerical examples demonstrate that the proposed estimator is comparable to and can even outperform existing multiply robust estimators.